Summary: The sky is falling for many Bitcoin miners - a perfect storm of collapsing Bitcoin price, rising interest rates, skyrocketing energy prices, and faltering equity markets. Another category of mining faced doom and gloom back in 2014, the precious metals miners. A widely unknown form of alternative financing called “royalty streaming” helped push gold miners through choppy waters, picking up the slack as the market financing source. These royalty streamers were led by Franco-Nevada, a little-known public company that’s valued at $25 billion today. Who will step up now and be the Franco-Nevada for Bitcoin miners?

Two million dollars invested turns into a billion dollars of return. A one million-dollar check generates over $100 million of gains. Is it Warren Buffett? Is it one of the many Midas List SaaS VCs? Is it crypto? Maybe Solana or Dogecoin??

None of the above.

This is the best investor you’ve never heard of, Franco-Nevada, and these are just two examples of returns they have made investing in precious metals mines over the last four decades, generating 38% annual returns over their first 18 years post-IPO and never looking back since. At the time of writing, Franco-Nevada’s ~$25 billion market cap is larger than software stalwarts like Twilio, Okta, Zoominfo and DocuSign. When asked about the key to Franco’s remarkable run during a 2002 interview, co-founder Pierre Lassonde attributed his success to “having a good feel for where metal is buried.”1

The world looks a little different today than when Franco-Nevada was started in the 1980s, but commodity cycles haven’t changed one bit. Like gold in 2014 and oil in 2020, Bitcoin is facing a bear market moment of reckoning. Bitcoin miners, specifically, are in a world of pain. Across the top 10 public miners, median stock price is down 87% since all-time highs in fall ‘21, wiping away ~$25 billion of aggregate market cap.

Miners are facing a triple-whammy, across their revenue source (dollars per Bitcoin mined) and two largest cost components, energy and hardware:

Bitcoin price is down 55% YTD and 70% peak to trough - $21k today versus $69k in November ‘21

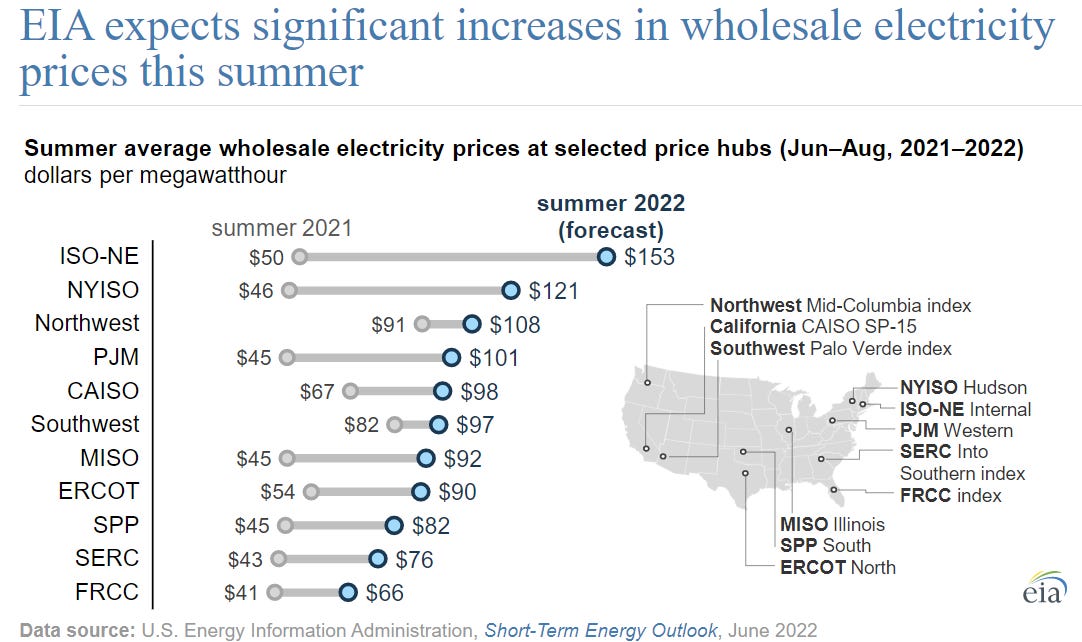

Continued inflationary pressure on energy price (80%+ of a miner’s variable cost) is crushing any miner who is subject to market-based pricing. Spotty energy availability is also causing miners in places like Texas to turn off mines during periods of excessive demand (like during heat waves). Many miners made decisions to build infrastructure around energy sources that were “cheap” last year, but have skyrocketed anywhere from 20% to 200% y/y since last summer (per EIA report from June, shown below).

Wholesale electricity prices are up in every single US market this summer, with some exceeding 3x y/y; per EIA

ASIC (computer chips used for mining) prices are down 50-70% since Nov ‘21 peaks, spelling deep trouble for miners who took on debt positions in 2021 collateralized by their Bitcoin holdings and/or ASICs.

On top of everything going on at the individual miner level, network hashrate2 (which indicates the difficulty of mining a single bitcoin - lower is better for miners) is down only ~15% from its all-time high in May and still up 17% YTD, making the fruits of miners’ labor still difficult to come by.

Certain miners will be forced to shut down facilities or even declare bankruptcy if Bitcoin remains sub-$20k for a prolonged period. The breakeven cost per Bitcoin mined ranges from ~$5-15k across public miners, but this figure often doesn’t include the additional capital needed every 2-3 years to refresh the mining chips. If the all-in cost of production exceeds the price of Bitcoin, margins quickly flip negative and miners will need bridge financing to survive. Short-term debt financing options to help ride out the storm are also limited, given existing high leverage and negative free cash flow for many public miners, combined with rising interest rates and low appetite from equity markets.

Bitcoin mining has broad implications for the crypto market overall. Miners have historically held onto their mined bitcoin each month with the expectation of rising prices, but some started to buck the trend in April and became forced sellers in anticipation of higher electricity costs and near-term liquidity needs. Core Scientific (top 3 public Bitcoin miner) sold 7,202 BTC (75% of its supply) in June and Bitfarms sold 3,000 BTC (almost half its supply) in May. These forced sales contribute to downward pressure on Bitcoin price and therefore the entire crypto market, so it’s worth understanding how mining works and the severity of the miners’ predicament.

Gold Mining vs. Bitcoin Mining

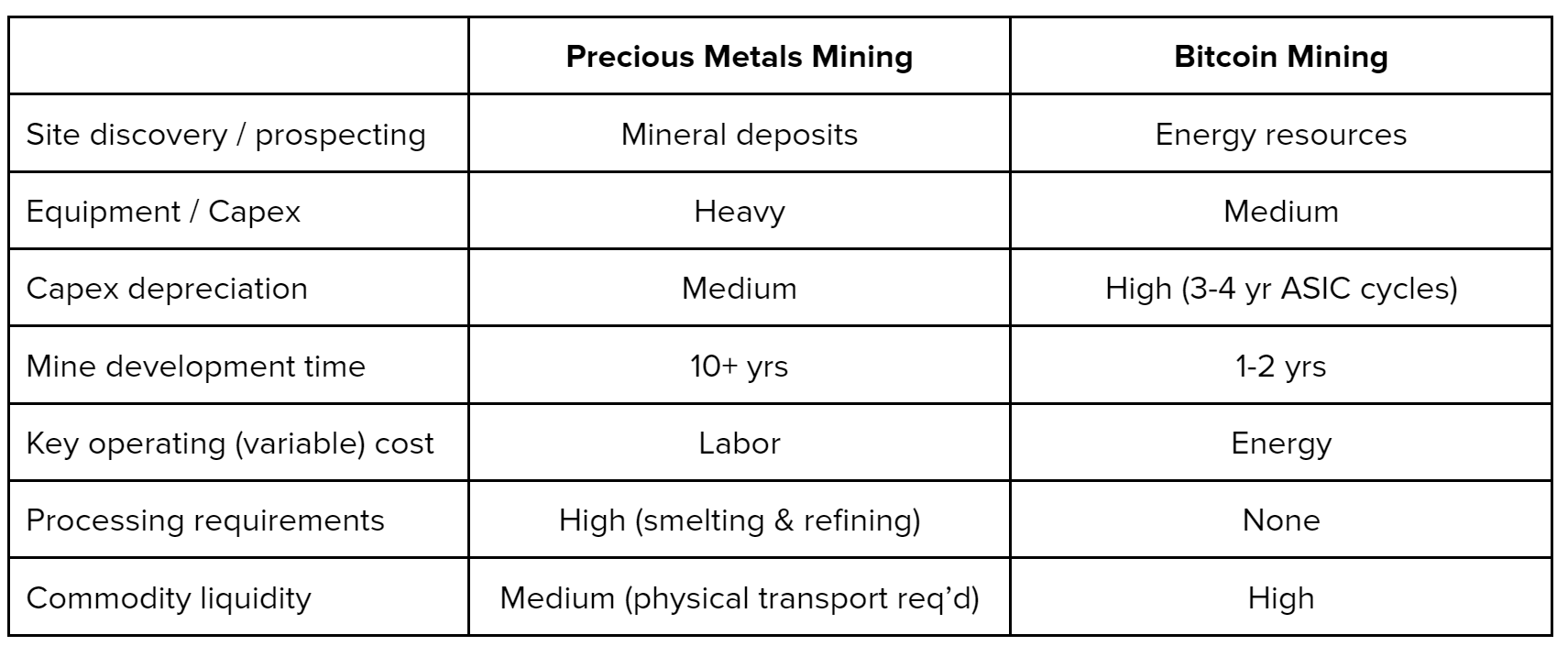

The media loves representing Bitcoin as “digital gold” and drawing comparisons at the asset level, but rarely do we dig a layer deeper to uncover the similarities and differences at the mining level. Like gold mining, Bitcoin mining starts with discovering a site, pulling together capital + people resources, building the extraction infrastructure, and ultimately harvesting the asset. But the devil is in the details.

Finding a Bitcoin mining site starts with identifying cheap sources of energy (like solar in Texas or hydro in China pre-ban), ideally in countries with Bitcoin-friendly regulatory environments. Traditional gold mining begins with geological surveying for specific mineral deposits in traditional mining. Once the site is discovered, both Bitcoin mining and gold mining require heavy upfront investment in capex. Bitcoin mining requires grid connectors, containers, computer chips, cooling equipment, etc., while gold mining needs explosives, machinery and picks for digging shafts or stripping pits. Both require hiring people to implement the capex, although Bitcoin mining requires far fewer bodies. Gold mining benefits from having longer depreciation cycles on machinery needed for ongoing operations, compared to Bitcoin mining’s short useful life for ASIC chips (due to high compute intensity required). Getting a gold mine up and running, however, requires a bit more patience compared to Bitcoin mining. Gold mines can easily take 10+ years until production begins due to permitting delays, power generation hookups, desalinization, water treatment, transport lines, toxic waste management - the list goes on and on. Bitcoin mines are quite simple in comparison and can often go live in less than 12 months (assuming ready-to-go energy connectors and no ASIC delays). Finally, gold mining requires post-mining processing (smelting and refining) before the commodity actually resembles those gold bars we all love, while Bitcoin is readily available / tradeable the moment it’s “unearthed.”

History doesn’t repeat, but it does rhyme

Gold was riding high in the wake of the Great Recession, rising from ~$700/oz in the summer of 2007 to ~$1,800/oz by the summer of 2011. Investors turned to gold as a safe haven asset and inflation hedge when the Fed started slashing rates during the financial crisis. The gold bull wave remained strong until 2013/2014, when the Fed began signaling a near-term end to quantitative easing (increasing rates and lowering the inflation outlook), so gold’s allure as an inflation hedge lost its luster. The siren call of attractive equity market returns (+13% in 2012 and +30% in 2013) also lured many investors away from gold and back into public equities.

Following the commodity downturn in 2014, many gold miners shifted their focus to reducing operating costs, cleaning up balance sheets, and returning cash to shareholders who had soured on the near-term commodities outlook. Many mining companies found it challenging to raise capital from either public equity or debt markets (and many didn’t want to have to sell stock at depressed prices) - the chart below captures the post-2013 issuance slowdown.

While the debt and equity markets dried up, a little-known category of alternative financing companies called “royalty streamers” surfaced to fill the gaps and keep gold miners chugging along. Let’s dig into the inner workings of this financial product for traditional metals mining and how Bitcoin miners can utilize it to weather their storm.

Streaming and royalties 101

In a world cluttered with an alphabet soup of complex financial products like CMBS, CDS, CDOs, CFDs, etc., royalty and streaming contracts are refreshingly simple. The “royalty streamer” provides cash upfront to a mining company for the right to buy future production at reduced prices. As discussed above, a mining company typically discovers a site where it believes there's gold, builds a mine, digs up the gold, and sells it. But a miner's revenue tends to fluctuate with the volatility of precious metals prices, since commodities like gold trade based on supply and demand (in addition to serving as a store of value). Commodity price volatility can become a huge issue for miners since mining costs and salary expenses are not directly correlated with commodity price, resulting in short-term mismatches between revenue and costs.

Therefore, miners can use a royalty or stream contract to exchange future production from individual mines for cash today, as a form of project finance and/or de-risking future production. Think of royalty streamers as VC firms taking stakes in individual mines - spanning asset types (gold, silver, copper, etc.), geographies (developed vs. emerging markets), and stages of development (just an idea vs. full-blown operational mine) - except their transactions are structured as revenue share agreements rather than equity ownership deals. A slightly better analogy is an Income Share Agreement or “ISA,” a growing form of college tuition financing where a counterparty pays a student an upfront lump sum for tuition, in exchange for a portion of the student’s future income for a set period of time. Miners use royalty & streaming deals3 for both primary metals (the metal they’re intending to mine) and byproduct metals (ex: when a copper mine yields a small amount of gold).

As an example of a specific royalty deal, Franco-Nevada invested $1 million into the Canadian gold mine Detour Lake in 1998 in exchange for 2% of the mine’s total future net revenue (structured as a royalty). The mine operator Agnico Eagle invested $1B of capital into the mine over the development period from 1998-2013 and stands to generate $1.2B in revenue this year, yielding ~$20-25m of revenue for Franco-Nevada (on top of the $109m they’ve already earned since 2013).

From a mining operator’s perspective, royalty streaming has certain advantages when compared to traditional financing. Miners are able to fund project development with a hybrid capital source (less dilutive than equity and more flexible than debt) and de-risk a portion of the project. The deals are also tied to a single mine, providing more targeted financing than traditional equity financing, which sells ownership across the company’s entire portfolio of mines.

The miners’ biggest downside is that royalty streaming can become exceedingly expensive if a mine outperforms expectations (via upside discovery / higher production), since the royalty streamer takes a fixed percentage of future production into perpetuity. This is why royalty streaming deals typically account for <10% of a mine’s total financing sources (with the balance coming from debt + equity), although this share can increase during periods with tighter capital markets.

Royalty streamers have found product-market-fit across economic cycles, leading to their emergence as a meaningful part of the mining value chain. The five largest public royalty streaming businesses today have a combined market cap of ~$50B, led by Franco-Nevada (~$25B), Wheaton (~$15B), and Royal Gold (~$7B). One way to measure the success of the royalty streaming model is to measure the evolution of the market caps of the largest public royalty streamers against the market caps of the largest gold miners over the last 15 years, as a proxy for relative importance in the gold mining value chain. The total market cap of the top 3 public royalty streamers started as ~8% of the top 3 public gold miners in 2008 and has marched up to 50% today. We can even quantify the value royalty streamers provide to miners. When Franco-Nevada announced a $600m streaming deal with Teck Resources (a major Canadian mining company) in 2015, Teck’s shares jumped 20% on the news. At the time, public markets analysts applauded the transaction for “helping shore up Teck’s balance sheet during a cyclical low in the commodity cycle.”

Being royalty has its perks

From an investor standpoint, royalty streaming is an incredible business model. The top public players boast metrics like 17x forward EBITDA multiples, 24x forward FCF multiples, 75% EBITDA margins, and 50% Free Cash Flow margins. Gold miners trade at a significant discount (median multiples of 6x EBITDA and 20x FCF), largely due to the business model’s much higher capital intensity. As a non-mining reference point, Google (arguably the best business model of all time) trades at a forward EBITDA multiple of 11x and FCF multiple of 17x with 40% EBITDA / 25% FCF margins.

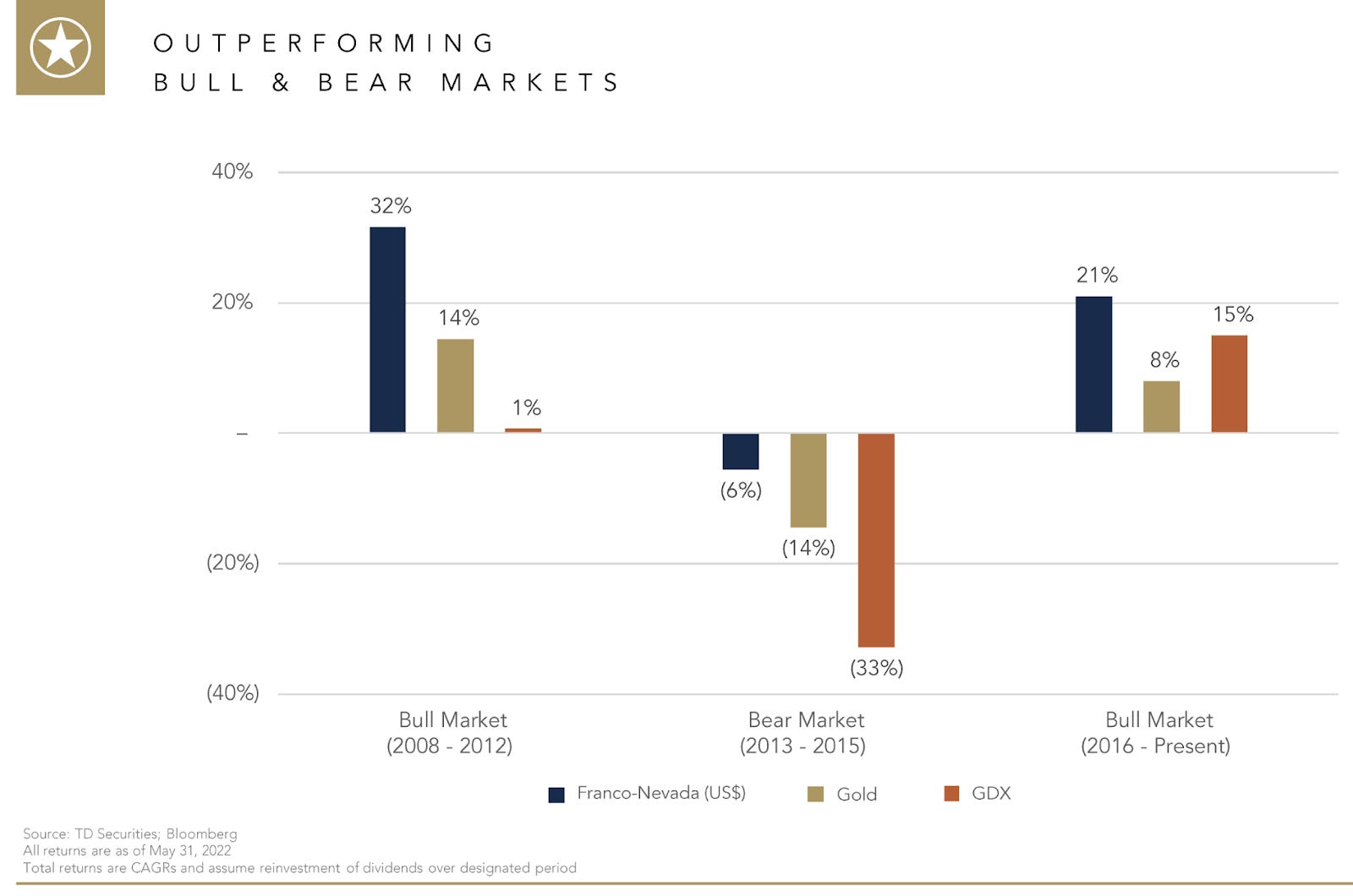

This valuation edge that royalty streamers hold over gold miners is not a flash in the pan. Since 2017, royalty streamers have held an average premium of 30-40% versus gold miners on a FCF multiple basis. Streaming stock prices have also outperformed gold miners across cycles, as shown below.

More specifically, the following slide from Franco-Nevada’s June investor presentation plots Franco’s total stock market returns against gold (commodity price) and the VanEck Gold Miner ETF (GDX). It’s quite clear who the winner is across cycles.

The royalty and streaming model resonates so well with public market investors because it provides asset-light exposure to commodity prices, while enabling a diverse, tailored asset portfolio. In many ways, royalty and streaming is a better business model than mining itself.

The royal crown: who wears it best?

The royalty and streaming model seems simple at face value, but many have tried and failed due to the difficulty of picking the best mines across the globe. The industry therefore remains highly consolidated: the top three players (Franco-Nevada, Wheaton, and Royal Gold) represent ~80% of the total market. But this “big 3” isn’t made up of equals — if Franco-Nevada is Lebron James, the others are more like JR Smith and Matthew Dellevadova. Or if we want to stick with the royalty bit, Franco is more like Julius Caesar versus Pompey and Crassus in the First Triumvirate. Like Caesar crossing the Rubicon, Franco-Nevada made a big gamble when they led the first known example of a precious metals streaming deal in 1986, investing $2 million in Nevada’s Goldstrike mine. And Franco was rewarded handsomely, turning that $2m into $1B+ of revenue since then — not quite the same as getting Rome, but certainly something to write home about.

Speaking of things to write home about, below are four FNV facts worth knowing:

283% stock price appreciation since 2011 - beating top gold miners, top royalty streamers and the S&P 500.

38 total employees run a company with ~$25B market cap, equal to ~$630m of market cap per employee.

Crunchbase did an analysis of tech company market cap / employee in Sept. ‘21 and Roblox led the pack at ~$50m, 12x lower than FNV (Roblox has since dropped down to $14m). Even public asset managers and REITs (who have more comparable business models to FNV) like Blackstone ($17m) Apollo ($14m), and American Tower ($19m) sit far below FNV.

100% recurring revenue stream, $700m in cash, and zero debt

Operating leverage (ability to grow revenue without increasing costs) so high that it almost seems fake

Why is Franco so good and why do they keep dominating their industry? Per insiders, their advantage stems from FNV’s decades-long focus on loading up with technical mining talent, rather than finance / structured products experts. The board has an all-star lineup of ex-C-suite execs (majority CEOs) from the largest mining companies in the world, like Newmont, Barrick Gold, Vale, Vedanta, and Rio Tinto. Nine out of the eleven Franco board members have degrees in geology / mining, including five PhD’s + master’s degrees. It’s no surprise that Franco can identify and pick the best projects — they’ve got dynamite while everyone else is still panning in the river.

What Bitcoin can learn from Old Man Nevada

Before dissecting how we can apply the royalty streaming model to Bitcoin miners, it’s worth briefly covering how Bitcoin miners have raised capital to date. Public miners traditionally issue public equity or debt. More than $2.5 billion of public equity was raised during the mining stock frenzy of 2021, and several new, creative ways for miners to use debt financing popped up. Many miners financed ASIC purchases by collateralizing the machines and financed operations by borrowing against their Bitcoin holdings.

In the words of Arcane Research, “To pursue the universal mine-to-hodl strategy, a miner must finance its operations with capital from outside the company, which is often debt secured by its bitcoin holdings. What will then happen if the bitcoin price plummets 80% in a few months, which it has on several occasions historically? In such a scenario, the companies who leveraged their bitcoin balance sheet can be in trouble and will not have the dry powder available to pursue opportunities like purchasing the assets of other mining companies with financial difficulties.”

This is the scenario unfolding before us today. Debt and equity issuance for Bitcoin miners has slowed down massively (lowest combined issuance quarter since Q3 ‘20, back when Bitcoin was ~$10k), and limited alternative financing options exist for miners today.

Who will be the Franco-Nevada of Bitcoin?

Like royalty streamers did in 2014 for traditional gold miners, the stage is set for alternative financing providers to fill the Bitcoin miner financing void. Product-market-fit for miners may be even higher with Bitcoin mining than traditional precious metal mining. Not needing to “discover” Bitcoin means the binary outcome risk of any single mine is greatly diminished. Bitcoin is a higher volatility asset than gold today, but the ability to structure streaming contracts with a floating discount offers some downside protection for the streamers. Bitcoin maximalists can also structure the deal with a fixed streaming price if they seek long-term upside (along with greater risk). With interest rates continuing to rise, the royalty streaming structure will become even more attractive for Bitcoin miners — miners are already paying 15-20%+ interest on their debt, and any defaults from overleveraged miners will impact credit ratings / lender appetite for the space broadly. Bitcoin royalty streaming offers a similarly enticing proposition for investors by providing diversified exposure across management teams / operators, countries with different regulatory regimes, energy sources / costs, mining chips, etc. — a “choose your own adventure” model of investing in miners.

Who can win this nascent market? This is the billion-dollar question. The winner(s) will likely come from one of three buckets: 1) Traditional metals royalty streamers; 2) Existing BTC-native lenders; 3) New BTC-native alternative finance startups.

Traditional royalty streamers have the business model nailed down for metals, but realistically are poorly positioned to enter the Bitcoin market. Not only do these companies have very little interest in straying from hard assets (per conversations with execs at large streaming companies), they also lack any subject matter expertise. Per a board member at a large public royalty streamer, “90% of these executives barely even know what Bitcoin is.” The analogy here would be betting on Pac Bell in the 90s to beat out Cisco at building computer networks solely because they previously developed phone lines. Someone like Franco-Nevada has spent decades understanding the minutiae of gold mining and hired a deep bench of industry experts, which is very difficult to port over to a digital asset like Bitcoin.

Bitcoin-native lenders like NYDIG, Galaxy Digital, and BlockFi (now part of FTX*) have emerged over the last few years to give miners debt financing options, and sound like a great fit on paper to launch royalty streaming products given their experience underwriting miners. While their existing miner relationships + cross-sell potential may give lenders a head start versus new entrants, they’re likely not a great fit for two key reasons. First, many centralized crypto lending platforms are struggling mightily in the current macro environment (read about the unraveling here), creating a window of opportunity for upstarts without lending baggage to enter the market. Second, BTC-focused lenders have focused so far on collateralized loans (either by bitcoins or ASICs) and getting into unsecured lending is an entirely different ball game. As a parallel, traditional metals lenders have largely avoided the metals royalty streaming business over the past 30+ years due to risk aversion and underwriting DNA that’s focused on downside protection.

Bitcoin-native alternative finance startups like Block Green*, Alkimiya, Blockstream, and River Financial benefit from not having to worry about cannibalizing an existing lending product. These companies are all taking slightly different approaches to solving the Bitcoin miner funding gap. Some are building product explicitly with the miner liquidity challenge in mind, while others are addressing it as a byproduct of their core offering. Another key split exists between a decentralized protocol-based approach versus a more traditional centralized counterparty offering. The pros of a protocol-based approach include easier access to retail capital sources and lower-friction ongoing capital raising; cons include regulatory headwinds and potentially a lack of centralized decision-making to choose individual mining projects.

Block Green (disclaimer: FF recently led the seed round) is building a decentralized lending protocol allowing renewables-powered Bitcoin miners to access revenue-based financing. The protocol lets bitcoin miners use their future Bitcoin production and existing hashrate (compute capacity from ASICs) as collateral for loans to finance mining investments, unlocking liquidity for miners. On the other end of the protocol, retail investors will be able to lend capital to the miners in exchange for a share of the future Bitcoin rewards produced.

Alkimiya is an open-source protocol for hashrate-backed contracts issuance, introduced in May 2021. The basics are as follows (see here for for in-depth details): Alkimiya launches a token (“Silica”) that represents a swap between a miner (or “blockspace” producer) who is selling future mining rewards produced by a specific amount of hashrate during the contract period, and the buyer who provides upfront payment in return for future cash flow yields from the blockspace (similar structure to Block Green). Miners use Silica to hedge against production risk / monetize their mining capacity, while investors get access to mining returns.

Blockstream, founded by the inventor of the proof of work algorithm that powers Bitcoin mining, offers a broad platform of crypto-financial infrastructure. Their most relevant product is the hashrate derivative token, which aims to offer broader retail investor access to their institutional mining business. Each note is backed by a set amount of hashrate and investors receive the bitcoin produced by the underlying hashrate over the next 3 years. Investors receive synthetic mining yield exposure, but since Blockstream is a first-party miner directly selling their own yields rather than a third-party market maker, Blockstream is missing out on the horizontal opportunity. Franco-Nevada’s history provides a lesson here: they started off as an independent company, were acquired by Newmont ($50B public gold miner) in 2002, and then spun back out in 2007 for $1.3B. FNV’s valuation has increased 20x since then because the value of a horizontal streamer is unlocked once they’re independent from a single miner.

River Financial is primarily a bitcoin brokerage for high net worth individuals (“HNWIs”) but also offers a “Bitcoin Mining as a service” product, effectively allocating HNWI capital into existing miner hosting capacity. This solves for providing retail (at least HNWI) exposure to mining yields and can de-risk some machine capacity for miners by guaranteeing runtime, but it does not necessarily de-risk BTC price exposure for miners.

Royalty streaming for Bitcoin mining presents a compelling win-win-win: miners get liquidity, institutional investors have a vehicle for bespoke mining yield access, and eventually retail investors will have an efficient way to access diversified mining returns (like FNV public shareholders have had for decades). But is this better achieved with a single counterparty (à la FNV) or a decentralized protocol? I believe decentralized platforms will be early winners due to their programmatic nature of underwriting (i.e. scoring based purely on quantitative factors like energy cost, ASIC cost, regulatory suitability of countries, etc.) that does not evaluate qualitative factors like mining operator team quality and other intangibles. However, when Bitcoin ultimately reaches steady-state pricing with lower volatility, the greatest winners in this category will be centralized platforms who can behave as more creative capital allocators. Franco-Nevada demonstrated the power of this model in the traditional commodity market by making the contrarian decision to enter Oil and Gas during the pandemic, which now looks like a stroke of genius (and likely wouldn’t have happened in a consensus-driven decentralized model). Regardless of the chosen approach, the Bitcoin mining industry needs royalty and streaming right now, and there is a tried-and-true precedent in plain sight. We’ll see if any of these up-and-coming protocols add efficiency without overcomplicating the core offering, or if the old ways will ultimately prevail, where all you need is someone who has a good feel for where the satoshis are buried.

*Founders Fund portfolio company

Thanks to Scott Nolan, Chase Lochmiller, John Luttig, Max Webster, Everett Randle, Sebastien Hess, and Matias van Thienen for their thoughts and feedback. Special thanks to Rayan Rafay for planting the seeds and Joubin Mirzadegan for nudging me along.

Note: price and network hashrate are not necessarily correlated - although hashrate may follow price in terms of short-term corrections, hashrate has been on a steady long-term upward march (regardless of BTC price volatility) since most ASICs eventually find themselves in the hands of more efficient miners who buy up the hardware owned by their less efficient (i.e. higher cost electricity) competitors. See here for a chart plotting network hashrate and price together.

The two deal types have slightly different structures:

Streaming deals are settled by the physical transfer of metal and typically focused on specific commodities produced by a particular project. In return for this upfront cash payment, the streaming partner secures a share of future production at an agreed-upon discounted price, which is either fixed or a floating percentage of the spot price.

Example: Franco-Nevada’s largest project Cobre Panama is subject to fixed payment streams of $437.37/oz of gold and a separate floating payment stream with an ongoing price per ounce of 20% of the spot price.

Royalty deals are settled with cash and typically based on overall project revenues; the royalty company never actually “sees” the commodities that the mine produces, but instead just receives a share of the revenue generated.